Thanks for your interest in my work! Currently, my KC Fed webpage is the best place to find my current research. The remainder of this page contains work that does not appear on that page.

Real Fluctuations at the Zero Lower Bound

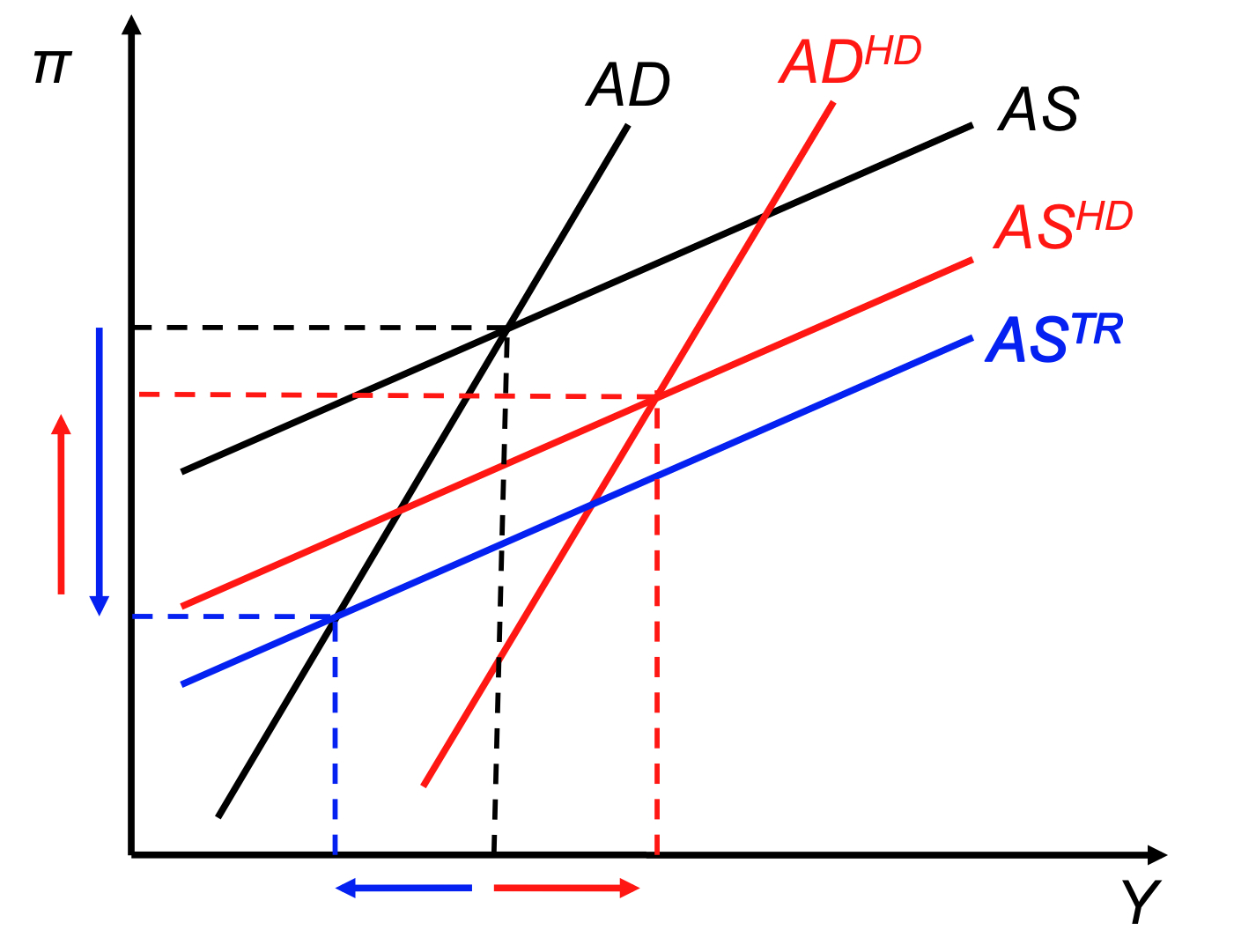

Aggregate

demand becomes upward sloping when the economy is stuck

at the zero lower bound. Thus, the economy may

respond very

differently to real shocks. A positive technology

shock which

shifts aggregate supply downward can cause a large

contraction in

output. However, these differential responses to

shocks emerge

when the central bank follows a standard Taylor rule (TR)

subject to

the zero lower bound. This rule implies that the

central

bank stops responding to the state of the economy at the

zero lower

bound. This assumption is inconsistent with the

recent behavior

by

monetary policymakers. The responses to shocks may

not

be so different if the

central bank follows a history-dependent

(HD) rule, which continues to respond the economy using

expectations

about future policy.

Discussion of Monetary Policy Slope & the Stock Market

By Andreas Neuhierl and Michael Weber

Midwest Finance Association Annual Meeting, March 2018

Discussion of Learning in the Oil Futures Market: Evidence & Macroeconomic Implications

By Sylvain Leduc, Kevin Moran, and Robert Vigfusson

Federal Reserve System Energy Conference, September 2017

Discussion of Oil Volatility Risk

By Lin Gao, Steffen Hitzemann, Ivan Shaliastovich, & Lai Xu

American Finance Association Meeting, January 2017

Discussion of Global Dynamics at the Zero Lower Bound

By William T. Gavin, Benjamin D. Keen, Alexander Richter, & Nathaniel Throckmorton

Federal Reserve System Macroeconomics Meeting, April 2014